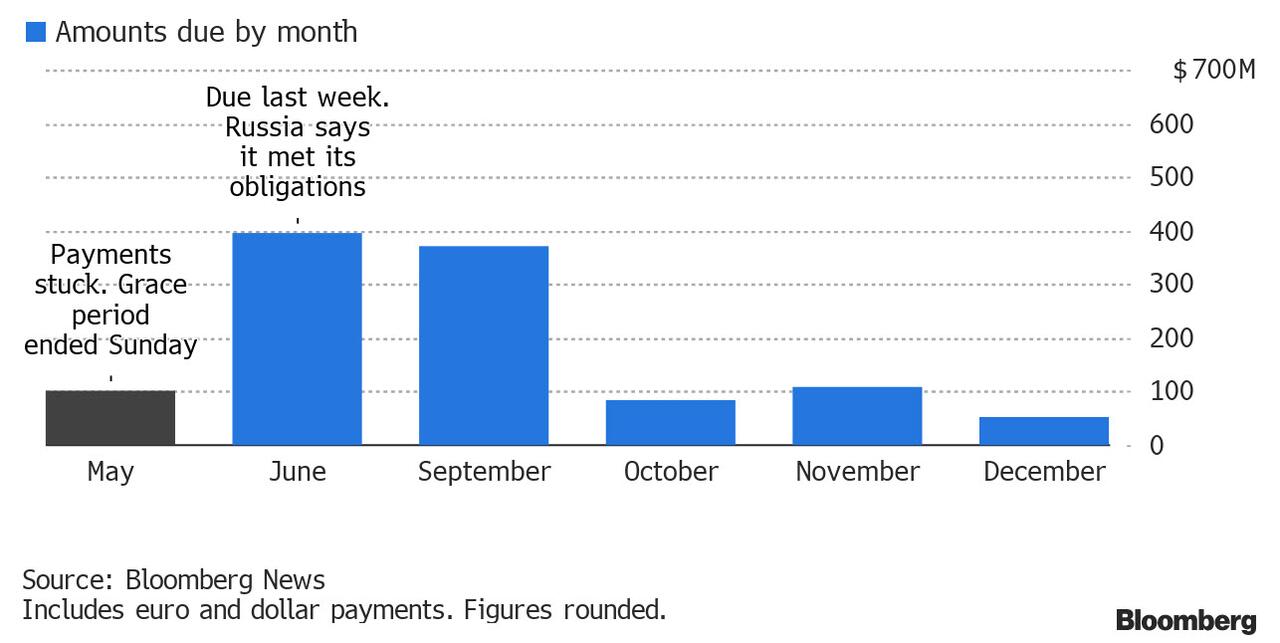

Russia on Sunday defaulted on its foreign debt for the first time since 1918 after the grace period on its $100 million payment expired, according to reports.

The $100 million interest payment deadline due to be met by the Kremlin had initially been set to May 27 but a 30-day grace period was triggered after investors failed to receive coupon payments due on both dollar and euro-denominated bonds.

Russia said that it had sent the money to Euroclear Bank SA, a bank that would then distribute the payment to investors.

But that payments allegedly got stuck there amid increased sanctions from the West on Moscow, according to Bloomberg, meaning creditors did not receive it.

Euroclear told the BBC that it adheres to all sanctions.

The last time Russia defaulted on its foreign debt was in 1918 when the new communist leader Vladimir Lenin refused to pay the outstanding debts of the Russian Empire during the Bolshevik Revolution.

President Boris Yeltsin’s government also defaulted on $40 billion of its local debt in 1998, when the country experienced a financial crisis but international aid helped the country to recover.

“It’s a very, very rare thing, where a government that otherwise has the means is forced by an external government into default,” Hassan Malik, senior sovereign analyst at Loomis Sayles told Bloomberg.

“It’s going to be one of the big watershed defaults in history.”

The default appeared to be inevitable after the U.S. treasury department last month decided not to renew a loophole that was set to expire on May 25, effectively stopping Russia from being able to pay its billions in debt back to international investors through American banks.

In response to that decision, Russia said it would pay dollar-denominated debts in rubles and offer “the opportunity for subsequent conversion into the original currency.”

Following the closing of the sanctions loophole, the European Union earlier this month sanctioned the Russian National Settlements Depository (NSD), stating that it “plays an essential role in the functioning of Russia’s financial system” and was ” thus directly and indirectly enabling the Russian Government in its activities, policies, and resources.”

The sanction of NSD effectively blocks Russia’s transfers out of the country.

For its part, Russian claims that it has the money to pay the debt and that the absent payment should not be considered a “default” because the Kremlin had made the payment but investors simply are not able to receive it, according to the country’s Finance Minister Anton Siluanov, who on Thursday branded the situation a “farce.”

Investors are unable to receive the payment because of two reasons, according to the finance minister.

“The first is that foreign infrastructure—correspondent banks, settlement and clearing systems, depositories—are prohibited from conducting any operations related to Russia. The second is that foreign investors are expressly prohibited from receiving payments from us,” Siluanov said, according to the RIA Novosti news agency.

“Everyone in the know understands that this is not a default at all,” RIA Novosti quoted him saying. “This whole situation looks like a farce.”

Last month, Siluanov again doubled down on his comments regarding Russia’s willingness to pay the debt, stating that the situation had been “artificially created by an unfriendly country” and that the default would not impact Russians’ quality of life.

Russia owes about $40 billion in foreign bonds. Prior to its war on Ukraine, the country had around $640 billion in foreign currency and gold reserves.

However, the majority of this was held overseas and has since been frozen in response to the invasion of neighboring Ukraine on Feb. 24.

This article appeared at ZeroHedge.com at: https://www.zerohedge.com/markets/russia-defaults-foreign-debt-first-time-bolshevik-revolution-amid-western-sanctions

![German Farmers and Truckers Protest Against Government’s ‘Green’ Plan to End Diesel Tax Breaks [VIDEO]](https://i1.wp.com/nordictimes.com/wp-content/uploads/2024/01/tractors-protest-germany.jpg?resize=440,264)

![Drought Issues with the Panama Canal Are Driving Up Prices for Consumers Worldwide [VIDEO]](https://i1.wp.com/www.finnewsnetwork.com.au/newssystem/2023/Img5_360_230814.jpg?resize=440,264)

![Is Africa Becoming The New Middle-East? [VIDEO]](https://img.youtube.com/vi/1CTyvDffUXs/hqdefault.jpg)

{kind=link}