What feeling do you have when you hear IRS? Is there a sick feeling in the pit of your stomach or do you just roll your eyes knowing that April 15th will be here all too quickly? Throw in the word audit and emotions and blood pressure can reach levels you never dreamed of.

Most taxpayers envision Internal Revenue Service audits as intrusive investigations resulting in criminal sentences. Today, nothing could be farther than the truth: The IRS’s auditing power has been greatly diminished in the past decade. IRS audit resources have been reduced by 28 percent in the last decade and the audit rate has dropped from 0.9 percent in 2010 to 0.5 percent in 2018. In fact, the number of IRS audits in 2018 (991,168) dropped by almost half compared to 2010 (1.735 million).

Since 2010, the IRS has been tasked with doing more with less resources, but the reality is that the IRS cannot do more audits with less resources. The IRS audit data reveals 10 trends from the past decade that have become the new realities for current state of IRS audits.

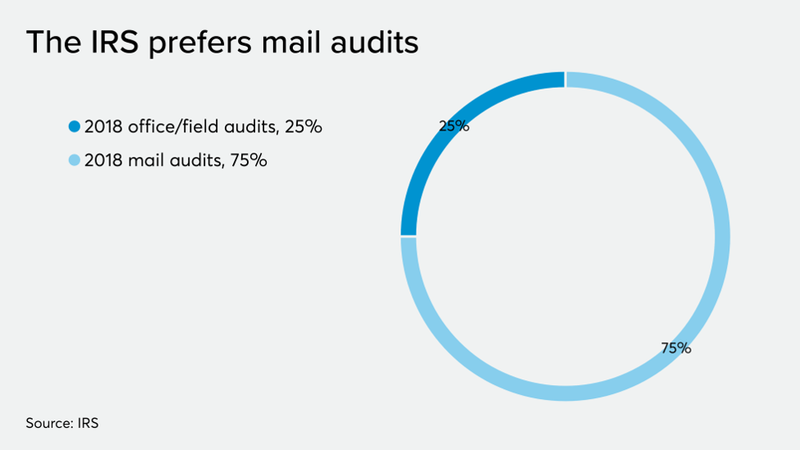

1. Most audits are done by mail

This trend started with IRS reforms in the late 1990s. In 1998, just before IRS reforms, the service audited 47 percent of taxpayers by mail. In the past decade, IRS data shows that the service prefers the less-intrusive mail audit. Today, three out of four audits of individual taxpayers are done by mail — a ratio that has held since 2010. These audits usually challenge small amounts of credits or deductions on a return, and require only a mail response, with documentation, to an IRS central campus location.

2. The main issue in audits: The EITC

Fifty percent of all individual audits involve a taxpayer who is claiming the Earned Income Tax Credit. IRS efforts to curb EITC errors largely rely on audits to hold a questionable EITC claim on a return. Politicians have criticized the IRS in the past for picking on low-income taxpayers, and the EITC audit rate is their main evidence. Compared to other taxpayer profiles, the IRS clearly has the propensity to address the EITC taxpayer more than other issues, even the small-business individual taxpayers. (See below for the trend on high wealth audits.)

3. An alarming amount of people do not respond to an audit

There is linkage here to the EITC mail audit. The Taxpayer Advocate reports that almost two-thirds of all mail audits go without response or are assessed by taxpayer default. That is, the IRS just assesses the additional tax without the taxpayer contesting the service’s determination. Only one in five taxpayers agree to their mail audit adjustment — and likely, from the data, they don’t understand how to appeal. This mess leads to many audit reconsiderations (i.e., an audit “re-do” request). Again, more question marks here for the targets of mail audits — the low-income population.

4. The most common IRS challenge to a return is not an audit

The dreaded CP2000 Automated Underreporter notice is current three times more prevalent than an IRS audit. The CP2000 program utilizes IRS information returns (W-2s and 1099s) to match them against the filed return to discover discrepancies. A discrepancy may result in a CP2000 notice proposing additional tax (and possibly penalties) to the return. Most taxpayers do not realize (or care, for that matter) that a CP2000 is not an audit. The CP2000 is less intrusive than an audit because the IRS is not allowed to examine the taxpayer’s books and records. For most taxpayers, however, the difference does not matter: The average amount owed for a CP2000 notice in 2018 was $1,773.

However, there is good news for taxpayers: Even the mostly automated underreporter process has been cut back due to lack of IRS resources.

5. The IRS knows who to audit

The audit change rate was 89 percent for all taxpayer types in 2018. In fact, the audit change rate has been between 81 percent and 89 percent since 2005. When the IRS selects a return for audit, they pretty much know it will likely result in an adjustment.

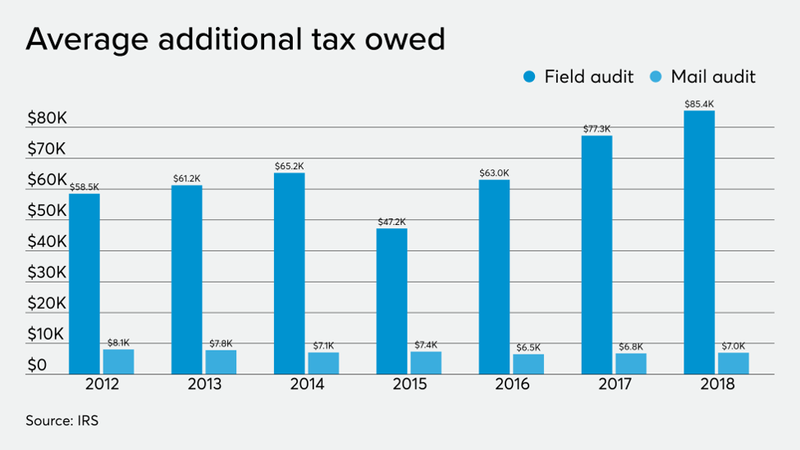

6. Field audits are rare, but expensive

In 2018, the IRS hit an all-time low for the number of field audits conducted. Field audits are the most comprehensive, and are saved for complex taxpayers and situations — like businesses and tax avoidance schemes. The IRS has said that their audits have a great return on investment and reduction of audit results in large amounts lost to the U.S. Treasury. The numbers support the IRS. In 2018, the average amount owed in a field audit was $85,400. Luckily for taxpayers, the IRS only conducted just under a quarter of a million field audits in 2018.

7. Want your business to escape audit? Be an S corp or partnership

The IRS continues to struggle to audit S corp and partnership returns. This situation is likely to get worse as the more experienced IRS business auditors continue to retire. Audit rates for S corps and partnerships are both 0.22 percent — or, put another way, one in every 455 passthrough entities were examined in 2018. It is no wonder that the number of S corporations have increased by 38 percent from 2005 to 2018 (3.5 million in 2005 versus 4.85 million in 2018).

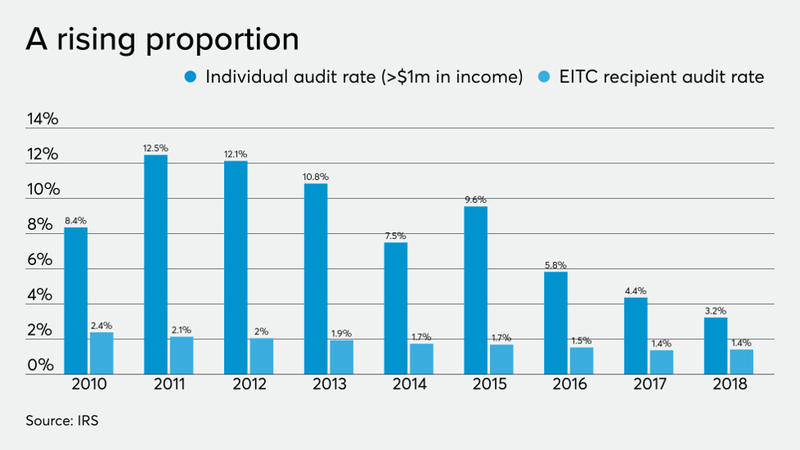

8. Audits on the wealthy are still popular, but have dropped

In 2011, one out of every eight taxpayers who earned more than $1 million in income were audited. In 2018, the number dropped to one in every 31 taxpayers. However, those who earn more than $1 million are still among the most popular audit profiles.

9. Audits have dropped, but penalties are still prevalent

The total volume of individual audits and CP2000 notices has dropped from 4 million in 2005 to 3.9 million in 2018. However, in 2018, 606,121 individual taxpayers were assessed the accuracy penalty for making an error on a tax return (audit or CP2000 notice). In 2005, that number was only 58,366. The moral here is if the IRS has to audit or send a CP2000 notice, it will now look to penalize errors to deter future noncompliance. The number of individual taxpayers with an accuracy penalty from an audit/CP2000 notice has increased 10 times since 2005.

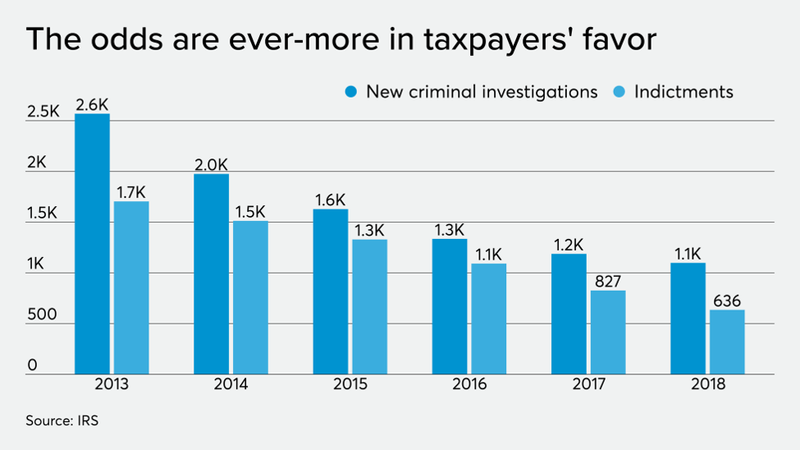

10. Tax evasion prosecutions are low

Finally, the “fear of an audit” myth buster. The IRS does not like to publish this statistic. In 2018, there were only 636 indictments of legal source tax crimes. IRS tax evasion criminal investigation cases have dropped by 58 percent since 2013. The main source of IRS legal source tax crime cases are IRS field auditors and criminal investigators, i.e., revenue agents and special agents. From 2013 to 2018, the numbers of revenue agents and special agents have decreased by 26 percent and 21 percent, respectively. As a result, the number of criminal investigations and indictments continue to decline.

Fear of an audit has always been a main driver for compliance with the IRS. The 2018 Realities and the IRS ability to close the tax gap. Comprehensive Taxpayer Attitude Survey continued to show that 63 percent of taxpayers cited fear of an audit as an influential behavioral factor for correctly filing and timely paying their taxes. The tax gap, as currently measured on 2011-2013 returns, shows that the Treasury loses $352 billion a year due to inaccurate tax returns. With the fear of an audit becoming a myth, how will the IRS close the tax gap?

As the fear of an audit motivator becomes less of a reality, the IRS must seek to simulate the audit by touching as many taxpayers as they can. For now, that looks like sending a lot of non-audit notices to taxpayers. Recently, the Treasury Inspector General for Tax Administration reported that the IRS sent over 219 million notices annually to taxpayers. In 2001, the number of notices sent was only 30 million. With the IRS’s current resources, the IRS notice may be the only means the IRS has to let taxpayers know that they are still there.

This article appeared at ZeroHedge.com at: https://www.zerohedge.com/personal-finance/10-major-trends-irs-audits