New data from the Federal Reserve detailing citizens’ net worth shows that the issue of being “left behind” has now spread to all Americans aside from the top 10%, according to Bloomberg. This means that even the upper middle class is starting to feel the pain of income stagnation. The growth of upper middle class income continues to lag behind that of those both lower and higher than them on the socioeconomic ladder, according to the data.

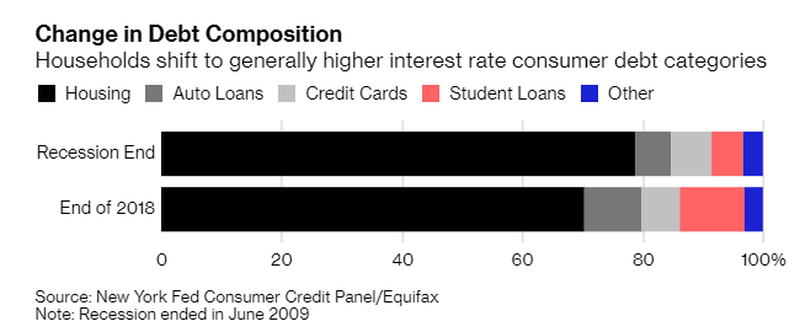

The cost of many items purchased by the upper middle class, including things like college education and cars, is outpacing inflation. That is causing upper middle class households to tap into more expensive forms of debt. The debt these households is taking on is shifting from mortgages to credit with higher financing costs.

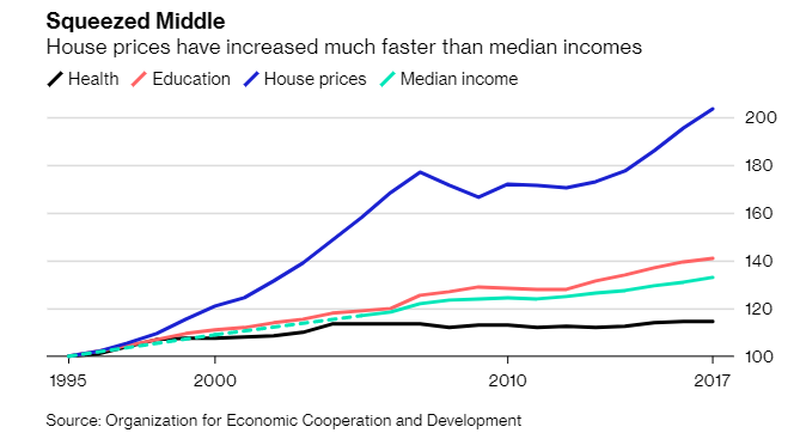

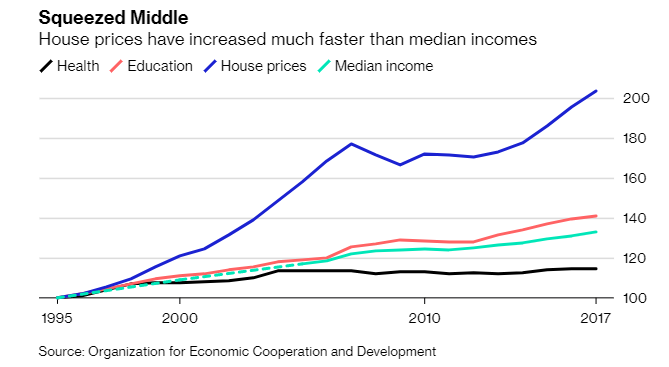

In addition, the overall middle class’ share of total income is falling while home prices have increased faster than median incomes.

The Organization for Economic Cooperation and Development said: “The middle class is increasingly only a dream for many. This bedrock of our democracies and economic growth is not as stable as in the past.”

Credit card rates recently hit a “generational high” despite the low prime rate. The spread between the prime rate and credit card interest rates is at its highest point in almost 10 years.

2018 property taxes rose by 4% annually, on average, according to an analysis of more than 87 million U.S. single family homes by ATTOM Data Solutions.

Todd Teta, chief product officer for ATTOM Data Solutions said: “Property taxes levied on homeowners rose again in 2018 across most of the country. While many states across the country have imposed caps on how much taxes can go up, which probably contributed to a slower increase in 2018 versus 2017. There are still many factors at play that can contribute to local property tax hikes, and without major changes in the way a community runs public services, tax rates must rise to pay for them.”

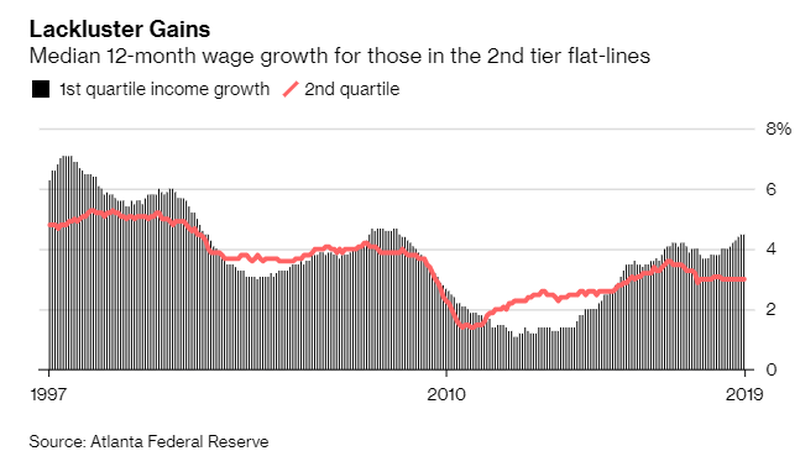

Only incomes in the top 25% were able to outpace this rate on an annual basis, according to the Atlanta Fed. For everyone else, a greater share of income must be allocated to property taxes, leaving less to spend on everything else.

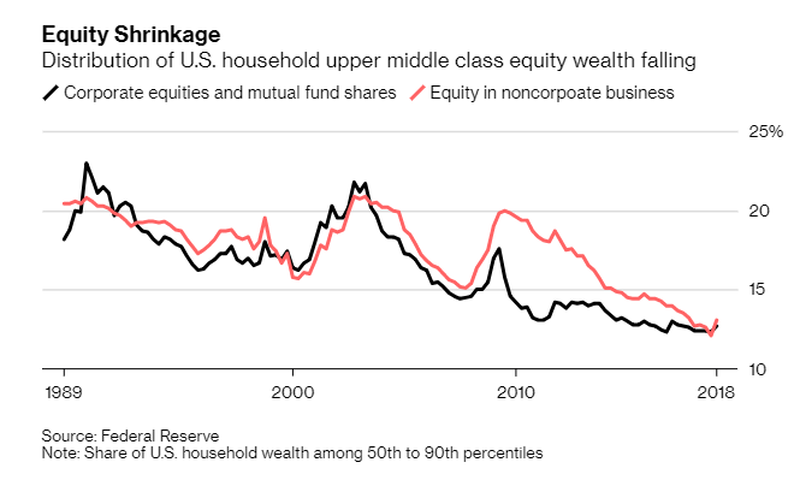

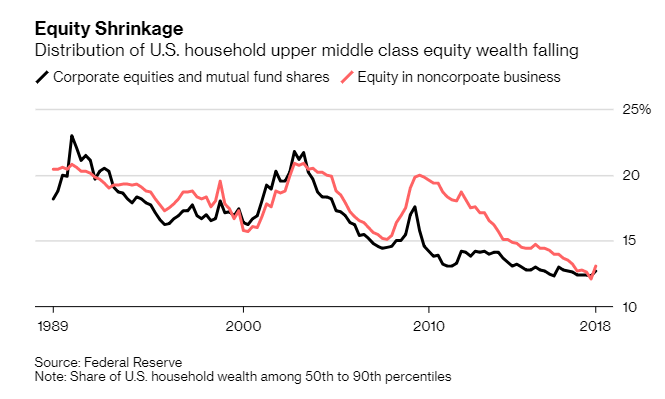

Equity ownership in companies, both public and private, is also sliding for the upper middle class. The share of equity ownership for citizens in the 50th to 90th percentile of net worth has fallen and the top 1% of Americans still own the majority of shares.

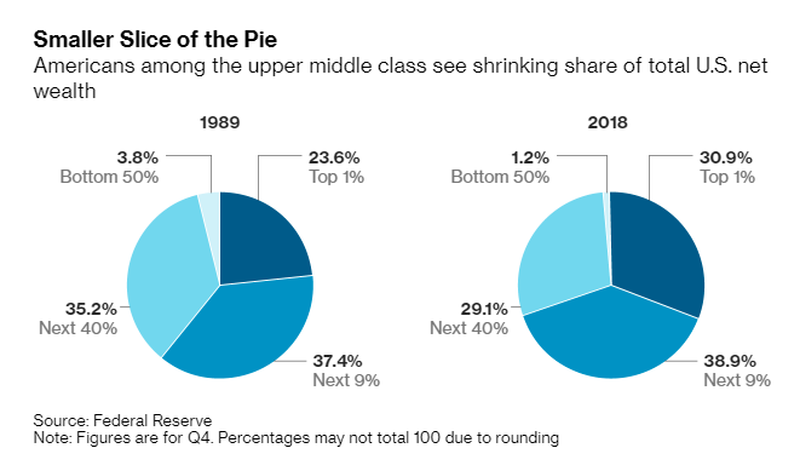

By the end of 2018, net worth as a share of the U.S. total had shrunk considerably for the upper middle class. During the course of just one generation, U.S. wealth held by households from the 50th to the 90th percentile fell from 35.2% of the total to 29.1%. Most of this wealth has been transferred to the top 1% of U.S. households.

The Organization for Economic Cooperation and Development has said that the middle class is “essential” for growth and countries where it thrives are healthier, more stable, better educated and have lower crime rates while boasting higher life satisfaction.

The OECD defines middle class as households with incomes between 75% and and 200% of the national median. Over the last 3 decades, incomes have increased 33% less than the average of the richest 10%, according to the OECD. Real income of the middle class has grown only 0.3% a year since the financial crisis.

Stefano Scarpetta, OECD director of employment, labor and social affairs said: “There is a risk of a spiral to the extent that the middle class is the one main sources of political and economic stability.”

{kind=link}

{kind=link}

{kind=link}

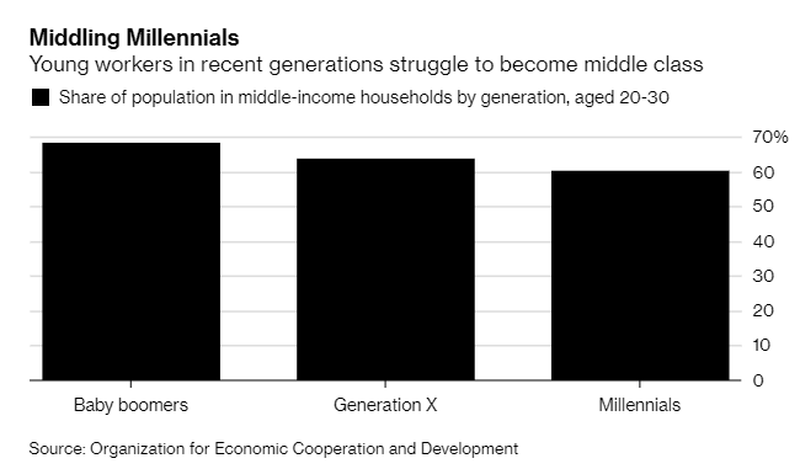

Rising to the middle class is also getting tougher. More skills are needed, as more than 50% of middle income workers are now in high skilled occupations, up from about 33% two decades ago.

“It’s a wake up call. Overall there is a need to really focus on targeted policy intervention for those with specific problems. General policies may not work very well,” Scarpetta concluded.

This article appeared at ZeroHedge.com at: https://www.zerohedge.com/news/2019-04-14/its-wake-call-7-charts-clearly-show-middle-class-being-left-behind