Things started moving very rapidly after President Trump ratcheted up trade friction with China on August 1 by announcing 10% tariffs on the remaining roughly US$300bn of imports from China to the US.

After markets first plunged realizing that the trade war was going to continue well into 2020 – and likely beyond the next presidential election – China initially responded by instructing SOEs (state-owned enterprise) to suspend imports of US agricultural products and then allowing the CNY (CNY is the ISO 4217 code for Renminbi, the currency of the People’s Republic of China) to devalue past the 7.00 level for the first time since 2008, as the trade war became a currency war.

Almost immediately, in response to the CNY devaluation, the US Treasury designated China a currency manipulator for the first time in 25 years under section 3004 of the Omnibus Trade and Competitiveness Act of 1988; the escalation remains open ended with policy makers indicating the potential for further retaliation, although no further tariff or non-tariff actions have yet been specified.

Meanwhile, China’s currency devaluation has resulted in a negative feedback loop, in which higher tariffs lead to more yuan devaluation, leading to even higher tariffs, and even more devaluation, and so on, until some exogenous events breaks this cycle.

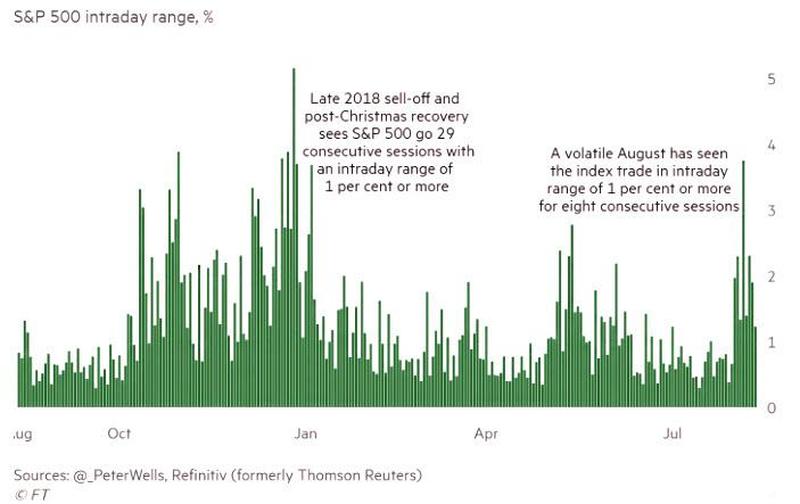

It is therefore not at all surprising that markets moved quickly to price in the ratcheting up of US/China trade tension, with the past 5 days resulting in the most violent moves in the stock market this year, with the biggest one day drop of 2019 followed by the most rapid three day rebound YTD. According to an FT analysis, the S&P 500 on Friday morning fell as much as 1.2%, marking the eighth straight session the index traded in an intraday range of more than 1 percentage point. It was the longest streak since a 29-day run that ended on January 10, when the market was convulsed by bouts of sharp selling and subsequent buying.

Yet while US stocks closed the week barely changed, down just 0.5% since last Friday’s close, China was less lucky and in just four trading days following the tariff announcement, Chinese offshore equities tumbled over 6%, Hong Kong equities dropped nearly to the same extent and the regional index fell 5.5%. The relative performance of the other regional markets was in line with their fundamental exposure to the trade factor, with the north Asian markets of Korea and Taiwan falling 3-5%, Australia (which is sensitive to China through commodity exports) declining 4%, and so on, with the ASEAN markets generally giving back 2-3%.

Trade concerns also cascaded through the currency markets, and the focal move was the 2% CNY weakening through the 7.0 mark for the first time in 11 years, which subsequently prompted the US Treasury to designate China a currency manipulator. The Korean won and Indonesian rupiah also declined over 2%, reflecting high macro sensitivity and carry-trade positioning unwind, respectively. The only regional currency to strengthen was the Thai baht.

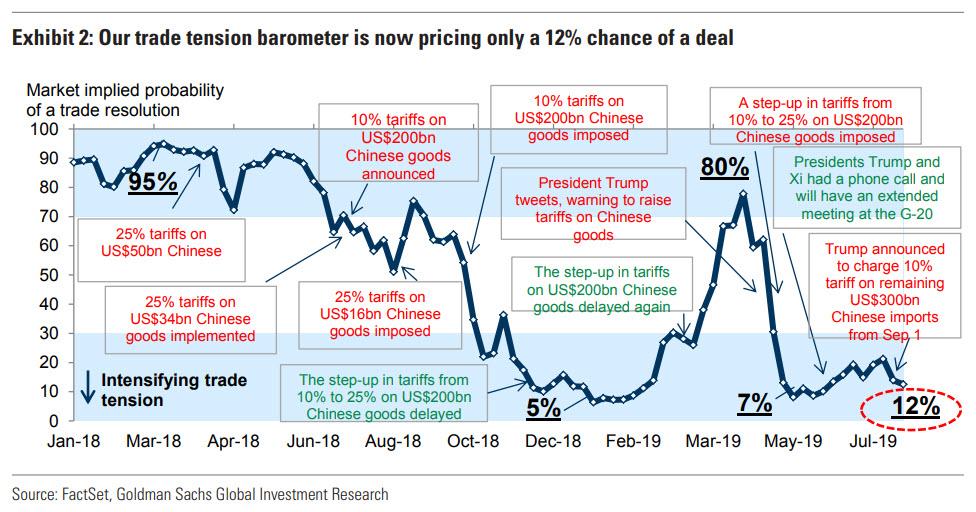

Finally, as a demonstration of the market’s now dismal view on trade relations, Goldman’s trade deal odds barometer (which was introduced less than two months ago) declined to pricing just a 12% probability of a trade deal compared with the recent post-G20 peak of 25%.

Even 12% may be optimistic, because as Bloomberg reports this morning, now that the trade war has shifted to a currency war, several former Chinese central bankers warned Saturday that there is no end in sight to the conflict between the world’s leading superpowers.

Chen Yuan, former deputy governor of the PBOC, said that the U.S.’s labeling of China as a currency manipulator “signifies the trade war is evolving into a financial war and a currency war,” and policy makers must prepare for long-term conflicts.

The U.S. currency-manipulation charge is part of its trade-war strategy, and it’ll impact China “more deeply and extensively” than the trade differences, Chen said Saturday. While China should try to avoid further expanding the disputes, policy makers must be prepared for long-lasting conflict with the U.S. over the currency.

And in a striking warning from the former central banker, he effectively admitted that dumping US Treasurys is certainly a possible retaliation: “The U.S. believes, in a geopolitical point of view, it’s being contained by China with China’s holding of its sovereign bonds,” Chen said,. “That means the U.S. is not completely without weakness.”

He also said that China should work to increase the use of the yuan in global trade such as the purchase of commodities.

Speaking at the same venue – the China Finance 40 meeting in Yichun, Heilongjiang – former PBOC Governor Zhou Xiaochuan said that conflicts with the U.S. could expand from the trade front into other areas, including politics, military and technology. He called for efforts to improve the yuan’s global role to deal with the challenges of a dollar-denominated financial system. Of course, the conflict that is most concerning is the military one. Luckily, that barrier has not been crossed yet, but it is only a matter of time before the US and China clash somewhere in the South China Sea with deadly consequences.

Sure enough, one of the other PBOC officials at the meeting signaled that tensions with the U.S. could increase. Zhu Jun, director of the PBOC’s international department, said “more ensuing measures are likely coming.” She didn’t elaborate.

Finally, ensuing that “more measures are coming”, the Communist Party’s flagship newspaper People’s Daily said in a commentary Saturday that the U.S. move is an “appalling” act to gain an advantage during trade negotiations and is doomed to fail.

Oh yes, and speaking of more devaluation – with Citi, JPM and SocGen now expecting the yuan to tumble to 7.35 or lower – Yu Yongding, a researcher at the Chinese Academy of Social Sciences, said in Yichun, said that while markets haven’t reacted too strongly to the weakening yuan this week, it is possible that “the yuan could weaken further on unexpected shocks in the future.”

This article appeared at ZeroHedge.com at: https://www.zerohedge.com/news/2019-08-10/former-chinese-central-banker-warns-beijing-may-dump-treasuries-retaliation

![German Farmers and Truckers Protest Against Government’s ‘Green’ Plan to End Diesel Tax Breaks [VIDEO]](https://i1.wp.com/nordictimes.com/wp-content/uploads/2024/01/tractors-protest-germany.jpg?resize=440,264)

![Drought Issues with the Panama Canal Are Driving Up Prices for Consumers Worldwide [VIDEO]](https://i1.wp.com/www.finnewsnetwork.com.au/newssystem/2023/Img5_360_230814.jpg?resize=440,264)

![Is Africa Becoming The New Middle-East? [VIDEO]](https://img.youtube.com/vi/1CTyvDffUXs/hqdefault.jpg)

{kind=link}